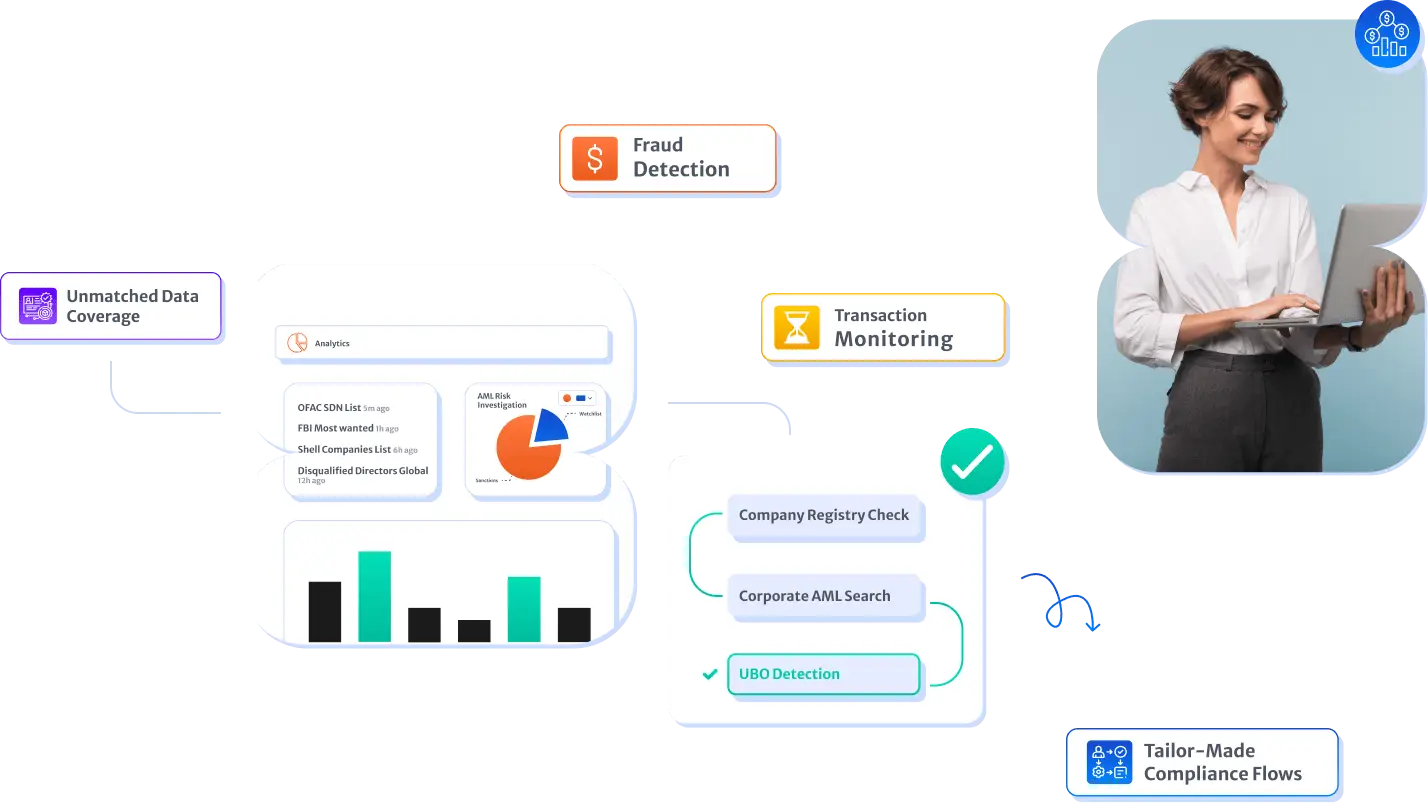

Why KYC Hub?

Because we deliver an integrated modular approach to compliance. Leverage our fraud & compliance infrastructure solution that enables you to manage the full financial crime lifecycle, offering seamless onboarding, monitoring, and dynamic risk detection in one comprehensive platform. Our cutting-edge solution streamlines your compliance processes, ensuring effective and adaptable risk management. Choose our all-in-one compliance solution for a powerful, adaptable, and efficient approach to managing your organization's financial crime risks.

AI-based fraud and compliance applications.

OpsFlow

No-code configurable platform to enable orchestrating identity, compliance, and decision flows for any use case.

Global Verification Portal

The building blocks to verify, understand, and monitor customers throughout their entire lifecycle.

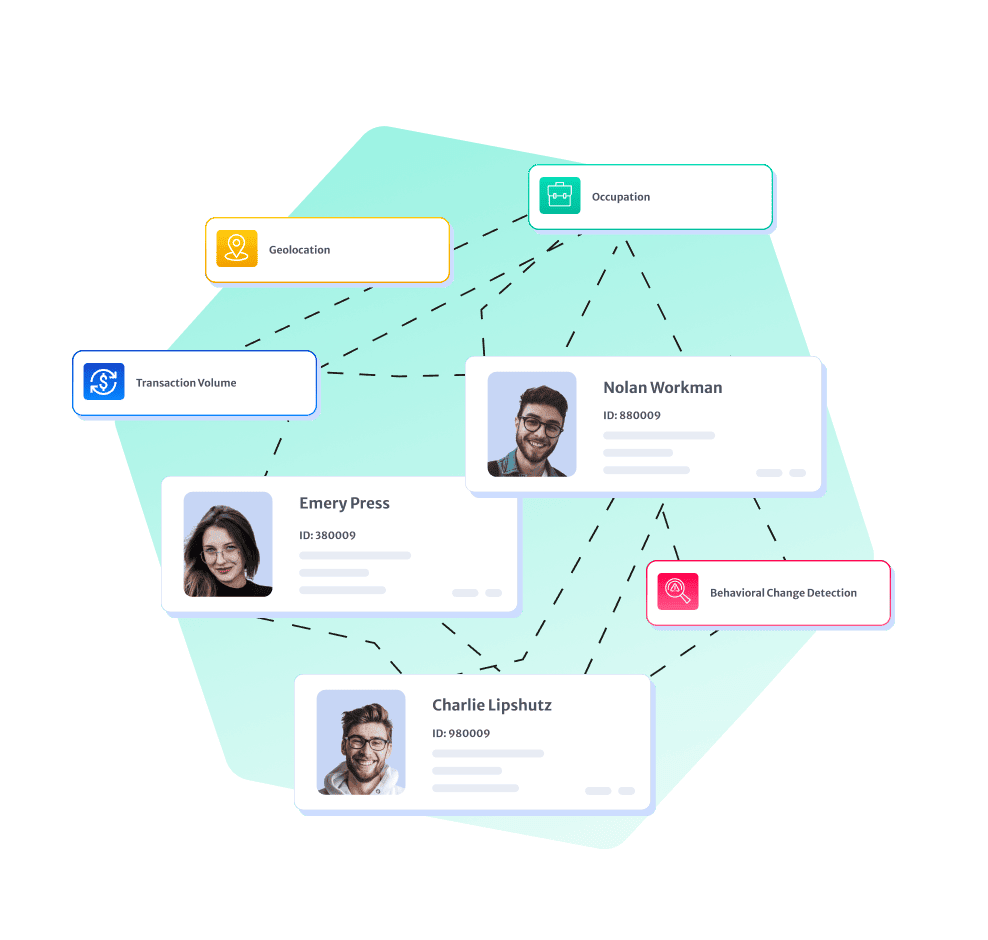

GraphIntel

Global knowledge graph of high-risk entities, with continuous updates and advanced risk detection.

Numbers That Speak for Themselves

Verification time end-to-end

Countries · 150+ languages

Reduction in compliance cost

Everything you need, in one platform.

[ VERIFICATION ]

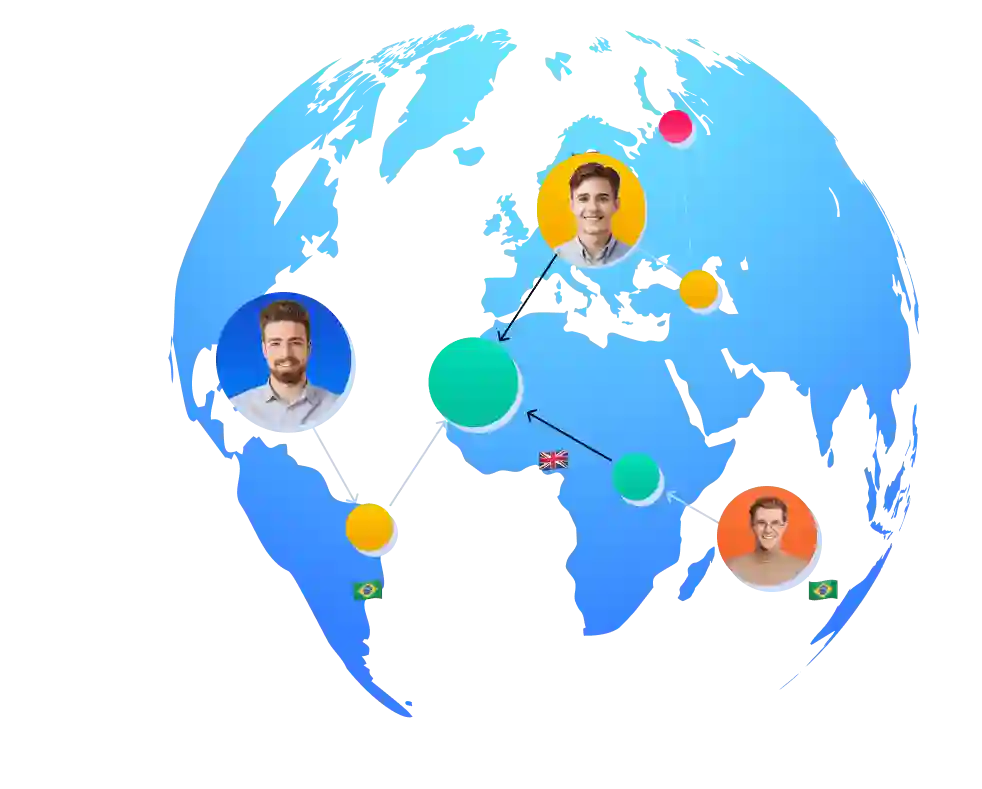

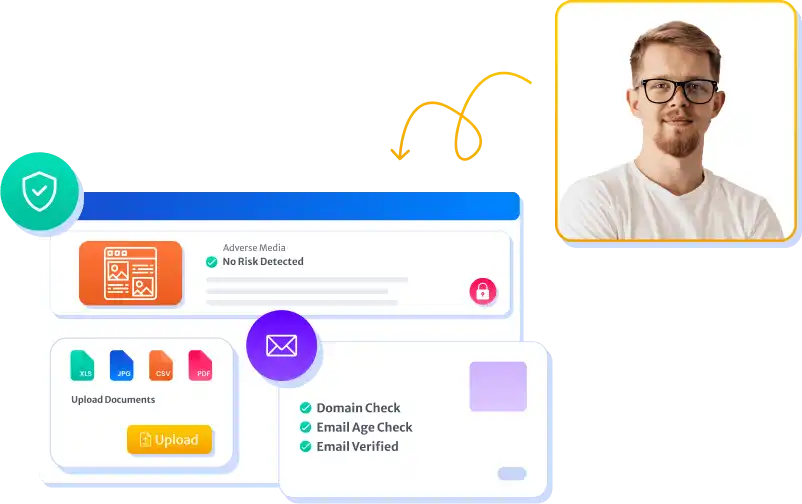

Global Verification Hub

Gain a competitive edge with swift global customer verification and painless onboarding through a variety of seamless methods. From identity and document checks to biometric liveness and business verification, every customer is onboarded in minutes with a single integrated stack.

Coverage across 190+ countries, 3000+ document types, and live registry data for businesses worldwide.

Book a DemoGlobal KYC

Real-time identity verification across 190+ countries.

Biometric Identity Verification

Liveness and face match for every customer.

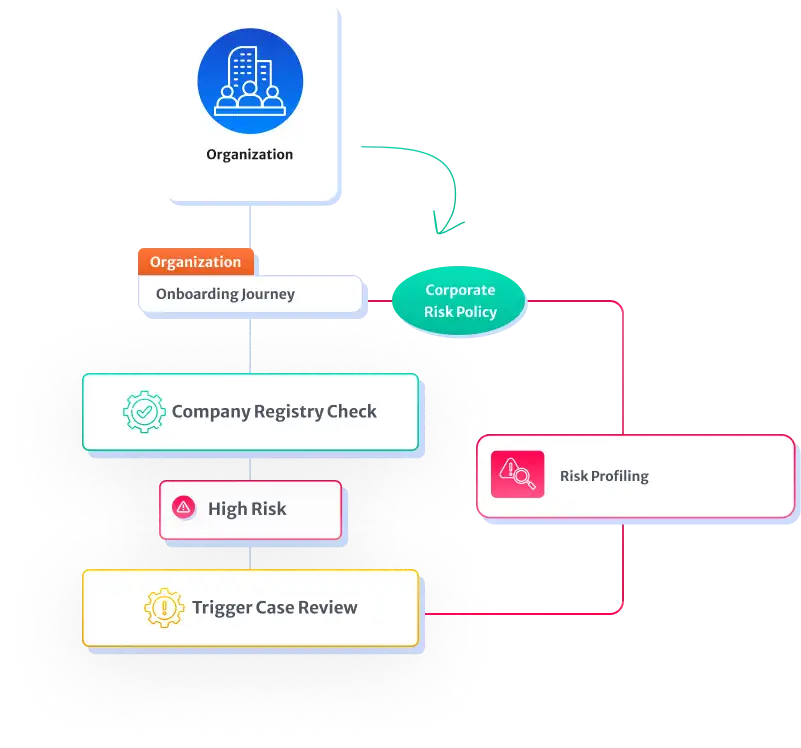

Global KYB

UBO discovery and live registry data on every entity.

Document Verification

Authenticate 3000+ ID types with deep forgery checks.

[ INDUSTRIES ]

Industry Specific Customised Offerings

Purpose-built compliance for the way your industry actually onboards, screens, and monitors risk — one platform, every regulated vertical.

Banking

Onboard retail and corporate clients, run CDD/EDD, and monitor transactions on one regulator-ready stack.

Learn more →Fintech

Launch in new markets fast with KYC, KYB, sanctions and fraud checks built for high-volume consumer onboarding.

Learn more →Payments

Onboard merchants, monitor flows, and meet PSP, PayFac and acquirer obligations across every corridor you serve.

Learn more →Lending

Verify borrowers, score risk, and surface fraud before disbursal — across consumer, SME and embedded lending.

Learn more →Insurance

Run distribution KYC, claims due diligence and sanctions screening across brokers, agents and policyholders.

Learn more →Crypto

Meet Travel Rule, screen wallets against on-chain risk, and onboard users with FATF-aligned KYC and KYB.

Learn more →Investment Management

Onboard investors and intermediaries, automate accreditation, and run perpetual KYC across the fund lifecycle.

Learn more →Trade Finance

Vet counterparties, screen vessels and dual-use goods, and uncover hidden UBOs across cross-border trade flows.

Learn more →[ USE CASES ]

Use Cases

Explore KYC Hub's diverse use cases — versatile solutions that cater to various industries and compliance needs, empowering businesses to mitigate risks and ensure regulatory adherence with confidence.

[ FRAUD ]

Adapt To Tackle Modern Day Fraud

Fraudsters' tactics constantly evolve, but KYC Hub and its dedicated fraud prevention team remain a step ahead. Working tirelessly to outpace fraud, we consistently invest in cutting-edge innovation to deliver the most advanced identity fraud prevention technology available.

- Stay ahead of fraud and money laundering

- Identify hidden risks

- Make smarter risk decisions faster

- End to end integrated compliance

- Build the flow that fits your use case

[ TESTIMONIALS ]

What our clients say?

KYC Hub exceeds all expectations, offering cutting-edge technology and top-notch service. Their system has drastically reduced our operational costs. Their robust data security protects sensitive customer information. We see KYC Hub not just as a provider, but as a strategic business partner.

Industry Insights

Read our latest blogs to dive into the world of compliance and uncover the latest insights, trends, and more.