How to Prevent Identity Theft: A Guide for Businesses

How to prevent identity theft, for a business, comes down to one thing. Stop a fraudster from passing as a real person at the moment an account is opened or a transaction is approved. Three controls carry that job. You need a written prevention program. You need layered identity verification underneath it. And you need liveness checks that defeat forged documents and the AI-generated faces now flooding onboarding flows. This guide walks through the warning signs, the regulatory obligations, and the verification stack that turns identity theft from an open door into a closed one.

Identity theft is the unauthorized use of someone's personal information for fraudulent ends. For the person whose data is stolen, it means drained accounts and a wrecked credit file. For the business on the other side of the transaction, it means an impersonator slipped through. That second loss is the one this article is about.

What is identity theft?

Identity theft happens when an unauthorized party uses another person's sensitive data to impersonate them or carry out fraud. The stolen details can include a name, Social Security number, date of birth, and financial account information. From there the damage spreads fast. Thieves drain bank accounts. They open new credit lines, hijack utility or insurance services, and file fraudulent tax returns in the victim's name.

A growing share of cases never touches a single real victim at all. In synthetic identity theft, a fraudster stitches together real and fabricated data, often a genuine SSN paired with a made-up name and address, to build a person who does not exist. That fake person plays the long game. The synthetic identity opens accounts and behaves normally to build credit. Then it "busts out," maxing every line at once before vanishing.

Identity theft vs. identity fraud

The two terms get used as if they mean the same thing. They do not. Identity theft is the act of stealing the personal, private, or financial information. Identity fraud is what comes next: using that stolen information to obtain money, credit, goods, or services. One is the break-in. The other is what the burglar does with the loot.

For a compliance team, both sit on the same control surface. If your verification stops the stolen identity from opening an account, you have prevented the fraud at the same time.

The scale of the problem

Identity theft is not a fringe risk. The Federal Trade Commission logged more than 1.1 million identity theft reports through its IdentityTheft.gov channel in 2024, and credit card fraud was the most reported type. New-account credit card fraud, where someone applies for a card in another person's name, far outnumbered misuse of existing cards. That single fact tells you where the front line sits. It is the application itself, the onboarding moment, the first verification a fraudster has to clear.

Synthetic identity is now the fastest-moving piece of the problem. Mitek and Datos Insights named it the defining fraud threat of 2026, and the technique now accounts for a large share of new-account fraud at banks and fintechs. The reason it spreads so fast is the supply chain behind it. Breached personal data is cheap. And generative AI now makes a convincing face or document in minutes.

Warning signs of identity theft

Catching identity theft early limits the damage. For consumers, the classic signals show up on statements and credit files. For a business screening applicants and customers, the red flags look different and appear earlier in the lifecycle.

- Unexpected changes in a credit score or unfamiliar accounts on a credit report

- Debt collection notices for accounts the named person never opened

- An application where the SSN traces to a different name or date of birth

- A device or IP geolocation that contradicts the stated address

- Multiple new applications sharing one phone number, address, or device fingerprint

- A document that fails authentication checks on fonts, microprint, or MRZ checksums

- A selfie that fails liveness analysis, suggesting a photo, screen replay, or deepfake

- Sudden change-of-address or change-of-contact requests on an existing account

How to prevent identity theft as a business

Prevention is layered. No single check stops every attack, so the goal is a stack of controls where a fraudster has to beat all of them at once. Here is what that stack looks like in practice.

Run a written identity theft prevention program

If you offer or maintain "covered accounts," U.S. law already requires this. The Red Flags Rule, built on Sections 114 and 315 of the Fair and Accurate Credit Transactions Act, obliges financial institutions and many creditors to maintain a written program that detects, prevents, and mitigates identity theft. The program has to identify relevant red flags, detect them in day-to-day operations, respond appropriately, and stay current as fraud tactics change. Treat it as a living document, not a binder that gets written once and shelved.

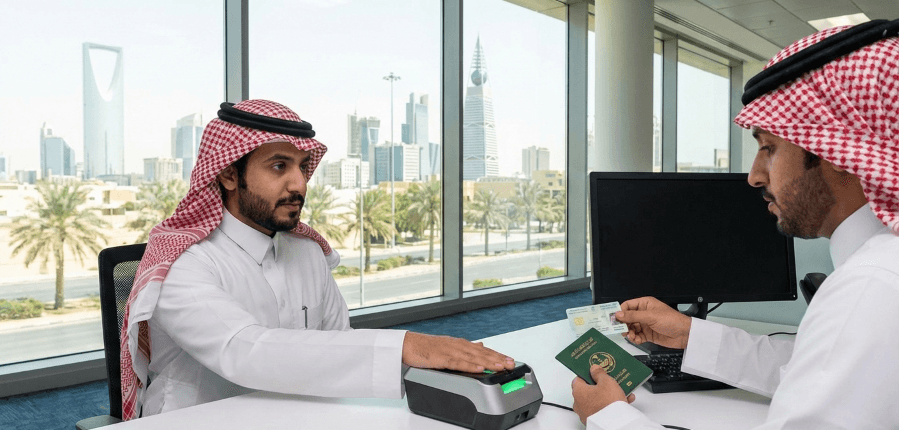

Verify identity at the point of entry

Your strongest moment to stop an impersonator is before the account exists. That is the job of a Customer Identification Program (CIP), the verification core mandated by Section 326 of the USA PATRIOT Act and FinCEN's rule at 31 CFR 1020.220. A CIP requires you to collect identifying details, then verify them by documentary or non-documentary means. Modern identity verification turns that legal requirement into a few seconds of automated checking instead of a manual review.

Layer document, biometric, and data checks

A single signal is easy to fake. Three are not. Document authentication confirms an ID is genuine and untampered. A biometric face match confirms the person presenting it is the rightful owner. Data validation cross-references the supplied name, date of birth, and address against authoritative sources. Run these together and a stolen credential without a matching live face gets stopped cold.

Defend against deepfakes with liveness detection

This is the control that separates 2026-ready verification from yesterday's. Liveness detection confirms a real, present human is behind the camera rather than a photo, mask, screen replay, or deepfake. Gartner has projected that by 2026 roughly 30% of enterprises will no longer trust identity verification and authentication solutions in isolation because of AI-generated deepfakes, which is exactly why liveness has moved from optional to load-bearing.

Apply risk-based friction

Not every customer needs the same scrutiny. A low-risk signup can pass through a light check. A high-value transaction or a flagged applicant, by contrast, gets stepped up to stronger proofing. Risk-based design keeps good customers moving and concentrates effort where the threat actually is.

Lock down internal data and access

Much identity theft starts with data your own business holds. Limit access to personal data to the staff who genuinely need it. Encrypt sensitive files. Enforce strong passwords and multi-factor authentication, and revoke access the moment an employee leaves. Train staff to spot phishing too, since a single harvested credential can open the door to everything behind it.

Book a demo to see layered verification stop fraud at onboarding

How synthetic identity fraud slips past basic checks

Synthetic identities are built to survive shallow verification. A made-up person with a real, valid SSN clears a simple database lookup because the number checks out. The name and the number have never been linked before, but a thin check does not test for that.

Catching synthetics takes correlation, not a single lookup. The questions that matter: does this SSN trace to this name and date of birth across multiple sources? Has this identity left any history before today? Do the device, email, and phone show the digital footprint a real adult would have, or were they all created last week? Layered ID fraud protection that scores these signals together is what exposes a fabricated person that any one check would wave through.

Identity theft on social media and through phishing

Social platforms are an easy harvesting ground. Public profiles leak the exact details that power impersonation and answer security questions. For your customers, the standing advice holds: tighten privacy settings, accept connections only from known contacts, avoid suspicious links, and use unique passwords per account.

For your business, the risk is account takeover fueled by that harvested data. The attack rarely looks technical. Phishing emails and smishing texts simply trick people into handing over the credentials or one-time codes that hand an attacker the keys to an existing account. Treat any inbound message that creates urgency around a payment or a login as suspect, and verify identity through a separate channel before acting.

How KYC Hub helps prevent identity theft

KYC Hub provides Identity Verification for global customers. It is built to confirm a real person is opening your account and not an impersonator or a synthetic identity. Several layers do that work. Facial biometrics and liveness checks defeat deepfakes and spoofs. Document authentication catches fraudulent and tampered IDs. And the verification flow is designed for frictionless onboarding rather than abandoned signups.

The same checks produce the audit trail your obligations demand. Reporting and compliance features capture the evidence behind every decision. And for high-risk transactions, enhanced security lets you step up scrutiny exactly where the threat concentrates. Because verification is fast and automated, the customer experience stays clean while the fraud controls run underneath.

That combination, strong proofing with a smooth path for genuine users, is what makes layered verification a prevention tool rather than a friction tax. Book an identity verification demo to see how KYC Hub stops identity theft at the point of entry.