Transaction Screening vs Transaction Monitoring: Key Differences

Compliance with anti-money laundering (AML) regulations is crucial in banking. Transaction monitoring and screening are prevention tools for financial crime, and where anti-money laundering is involved, transaction monitoring is the main focus.

On the other hand, transaction screening goes through a wide analysis and scrutiny of the transactions to look for any suspicious or prohibited activities before it approves the transactions, thus providing early mitigation.

This divide forms the basis of a comparison between, amongst other topics, transaction screening, and transaction monitoring while highlighting the different functions as key contributors to the enhancement of anti-money laundering processes.

Transaction Screening Vs Transaction Monitoring

The blog difference between transaction screening and transaction monitoring explores a detailed discussion of both methods, the differences in techniques, uses, and impact on AML compliance.

What is Transaction Screening?

Transaction Screening is a proactive compliance strategy used by many financial and non-financial firms to prevent financial crimes. It entails real-time screening of transactions against specified watchlists, sanctions lists, or particular criteria to intercept and identify potentially illegal transactions as they occur.

This technique is essential to anti-money laundering (AML) and counter-terrorism financing (CTF) programs, which discover and report suspicious activity such as securities fraud and terrorist funding.

Key Features of Transaction Screening:

- Real-Time Processing: Transaction screening occurs in real-time, giving rapid notifications when possible matches with sanctioned or politically exposed individuals (PEPs) are found, allowing for quick action to limit risks.

- Comprehensive coverage: It comprises pre-transaction screening, continuous transaction monitoring, and the integration of internal and third-party risk information. This thorough method aids in the identification of businesses or persons subject to legal limitations or engaged in questionable activity.

- Regulatory Compliance: Transaction screening is required for many businesses, including banks, financial firms, and cryptocurrency exchanges. To comply with global and regional AML requirements, these organizations must include effective screening methods in their KYC processes.

Challenges and Benefits:

- Challenges: Institutions using transaction screening confront several issues, including maintaining systems up to speed with the latest regulatory developments, controlling false positives, and ensuring efficient system settings.

- Benefits: Transaction screening increases the efficacy of financial crime prevention techniques. It serves as a first line of defense, preventing transactions involving high-risk parties and decreasing the effort on transaction monitoring systems by identifying obvious situations of compliance risk.

Transaction screening promotes regulatory compliance and protects the financial system from a variety of financial crimes, such as money laundering and terrorism funding. Institutions may prevent themselves from unintentionally aiding unlawful activity by putting in place appropriate screening measures.

What is Transaction Monitoring?

Transaction monitoring is a sophisticated surveillance system that detects and prevents financial crimes, including money laundering and fraud. It involves the examination of clients ‘actions, such as deposits, withdrawals, transfers, etc., in an effort to identify suspicious patterns that may lead to unlawful activities. Such a procedure is necessary for financial institutions to provide anti-money laundering (AML), and it is obligatory in many spheres of the business.

All in all, the following key features can be highlighted for transaction monitoring:

- Continuous surveillance: Transaction monitoring is an ongoing procedure that requires the analysis of transactions in real time and, at the same time, looking at past transactions to check for suspicious activities.

- Risk-Based Approach: The systems are applied and adjusted to the affiliated risks of the institutions, employing a risk-based approach for customers and their transcendent transactions. This strategy requires more work on customers that are marked as high-risk.

- Advanced Technology: Transaction monitoring systems, even when handling enormously large data, through artificial intelligence and machine learning, can capture fraudulent patterns and activities that older generations of systems might miss.

Transaction monitoring systems are an essential aspect of any financial system, mainly because they help the client’s institution in the management of risks, and they offer valuable information about client activity. These systems are helpful in the fight against financial crime as they are implemented in response to new threats and compliance changes.

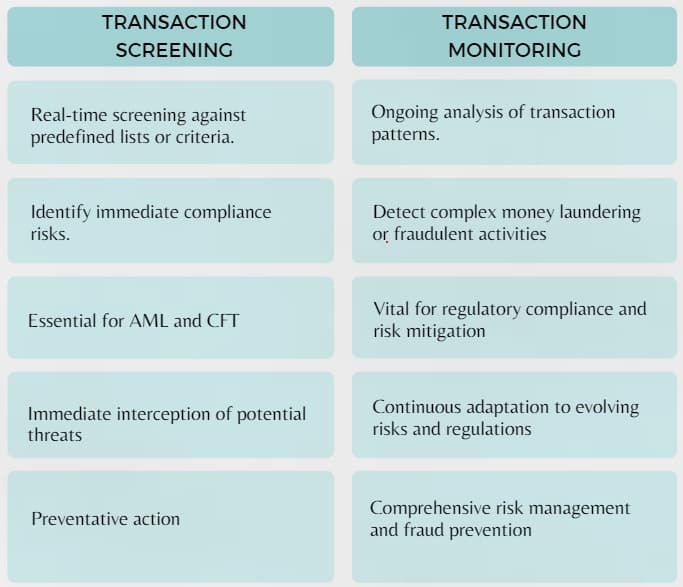

Transaction Screening vs Transaction Monitoring

As institutions navigate the complexities of AML compliance, the differentiation between transaction screening and transaction monitoring emerges as critical. Here are some significant distinguishing points:

Primary Focus and Timing:

1: Transaction Screening: Mainly concerns itself with the intra-day validation of transactions against watchlists, sanctions lists, or criteria of concern. The goal behind this process is to find immediate matches with the entities or people that can be classified as compliance risk.

2: Transaction Monitoring: Concerns the constant, live or reverse, or batch examination of transactions for sophisticated, staged money laundering or fraudulent schemes. It is intended to detect anomalies that require additional examination.

3: Purpose and Compliance: Both tools are instrumental to AML and CFT activities, which are targeted at minimizing the chance of financial fraud and staying compliant with the laws.

It is different from transaction screening, which is a preventive measure since it intercepts potential threats before transactions are made to prevent them. Transaction monitoring provides wider coverage since it analyses patterns as they go on until the concealed risks are detected.

4: Operational Integration: Using the two, transaction screening and monitoring provide an avenue through which financial institutions can be assured of meeting the infinite security and compliance demands. Transaction screening provides on-the-spot reactive measures to specified risks, while transaction monitoring gives a more profound and dynamic analysis of the current and future risks and regulatory compliance.

Introducing these processes guarantees that institutions will have a holistic approach to fraud prevention as well as to managing and preventing AML/CFT.

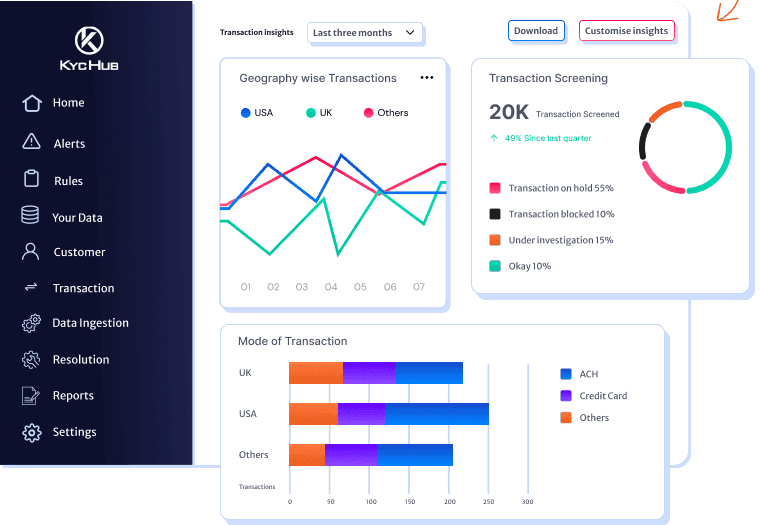

A visual representation of transaction monitoring vs transaction screening:

Impact on AML Compliance

Transaction screening and monitoring are critical for guaranteeing anti-money laundering (AML) compliance across financial institutions. These procedures are more than simply legislative obligations; they are critical weapons in combating financial crime, such as money laundering and terrorism funding.

Key Contributions of Transaction Screening and Monitoring to AML Compliance

1. Regulatory Compliance and Risk Mitigation: AML rules need both transaction screening and monitoring to prevent illegal financial transactions. Institutions that adopt these procedures may avoid the severe costs and legal ramifications connected with non-compliance.

2. Advanced Technology Integration: Solutions like Shufti Pro use AI and machine learning to improve the accuracy of identifying suspicious behaviors with advanced algorithms and real-time data analysis. This eliminates false positives while increasing the overall efficiency of the AML monitoring process.

3. Comprehensive Security Measures: The integration of various technologies and methodologies, including data mining, anomaly detection, and consortium data intelligence, equips institutions to adapt to complex money laundering tactics, thereby enhancing their AML strategies.

These systems collectively help maintain a robust AML compliance framework, which is crucial for the integrity and security of financial operations globally.

Challenges and Best Practices

Fintech companies and neobanks face unique operational challenges, significantly heightened during the COVID-19 pandemic, making them targets for criminal exploitation. Here are several Challenges in Transaction Screening and Monitoring:

1: Customization and Integration Issues: Transaction monitoring systems often have pre-set rules that may not align with specific institutional needs, leading to missed suspicious activities. Customizing these rules to fit an institution’s unique risk profile is crucial.

2: Data and Technology Challenges: AI’s effectiveness in transaction monitoring heavily depends on the quality and integrity of data. Poor data quality can severely impact the performance of these systems’ performance.

Static, rule-based monitoring systems are often outmaneuvered by sophisticated criminals who tailor their actions to remain under detection thresholds.

3: Regulatory and Compliance Challenges: Different regulators may have varying requirements and views on the practices for transaction monitoring software, complicating compliance efforts.

Continuous updates and understanding of regulatory changes are necessary to avoid penalties and ensure compliance.

Best Practices for Effective Transaction Screening and Monitoring

Enhanced System Configuration and Regular Updates:

- Implement robust transaction monitoring software capable of handling real-time analysis of millions of transactions to detect suspicious activities effectively.

- Regularly update and optimize the system configurations to enhance functionality and compliance with current regulations.

Advanced-Data Management and Reduction of False Positives:

- Develop strategies to manage and ensure the accuracy, completeness, and quality of data used in transaction screening.

- Focus on reducing false positives, which can cause backlogs and inefficiencies in the system.

Risk-Based Alerts and Continuous Review:

- Employ risk-scoring mechanisms to assign risk levels to customers, which helps prioritize alerts and focus on higher-risk activities.

- Continuously review and refine the rules, scenarios, and methodologies used in the transaction monitoring systems to keep them effective against emerging threats.

Conclusion

We hope this transaction screening vs transaction monitoring was insightful for you! Integrating advanced technologies such as AI and machine learning in these processes has further refined the effectiveness of AML strategies, reducing false positives and adapting to evolving threats. The challenges highlighted, from data quality to regulatory adherence, underscore the importance of continuous improvement and customization of these systems to meet specific institutional needs.

Contact KYC Hub for advanced Transaction Monitoring Solutions for those seeking to enhance their transaction monitoring capabilities. At the heart of these efforts is the unwavering commitment to safeguarding the integrity of the global financial system, making the thorough understanding and application of transaction screening and monitoring more crucial than ever.