KYC Challenges: The 6 Biggest Compliance Hurdles and How to Solve Them

KYC challenges are the operational and regulatory obstacles compliance teams hit while verifying customer identities, screening for risk, and keeping records audit-ready. Six come up again and again: high compliance costs, slow onboarding, identity verification friction, fragmented screening, sanctions exposure, and ultimate beneficial owner (UBO) discovery. None is unsolvable. A risk-based program with the right automation on top handles each one.

For banks and fintechs, these problems almost never show up one at a time. One onboarding flow might stall on document capture, throw a false-positive sanctions hit, and then leave a gap in the audit trail, all in the same session. This guide walks through the six challenges that cost compliance teams the most time and money, plus the controls that fix each.

What Makes KYC Challenging for Banks and Fintechs?

Know Your Customer is how a regulated business verifies who its customers are and weighs the financial crime risk they carry. The principle is simple. Execution is not. Requirements differ by jurisdiction. Customer data is messy and incomplete, fraud techniques outrun static rules, and every step has to be defensible to a regulator months or years later.

What results is a structural tension. Teams are asked to onboard customers fast enough to keep the business growing, yet screen thoroughly enough to keep financial criminals out and examiners satisfied. Most KYC challenges live inside that gap.

Challenge 1: High Compliance Costs

KYC is expensive. Headcount for manual review, licensing for screening data, remediation after a failed audit, and the periodic refresh of existing customers all add up. At a smaller institution, building and staffing a defensible program can cost about as much as the revenue that program is there to protect.

The lever is automation that removes manual touchpoints instead of adding another tool to babysit. Run document capture, data extraction, and screening straight-through for low-risk customers, and analysts only handle the exceptions that genuinely need judgment. That moves your spend off repetitive review and onto the high-risk cases where a human actually adds value.

Challenge 2: KYC Onboarding Challenges

Onboarding is where the friction really bites, and it bites the compliance team and the customer alike. Collecting documents, verifying them against reliable sources, running checks, routing exceptions: any one of these can stretch a process that should take minutes into days. And each extra step makes it more likely a legitimate customer simply gives up and walks.

A strong customer onboarding flow treats verification as one orchestrated sequence, not a chain of disconnected handoffs. Identity capture, document validation, screening, and risk scoring feed a single decision. Low-risk applicants clear automatically. Only edge cases escalate. Verify thoroughly, but don't make approval feel like an interrogation.

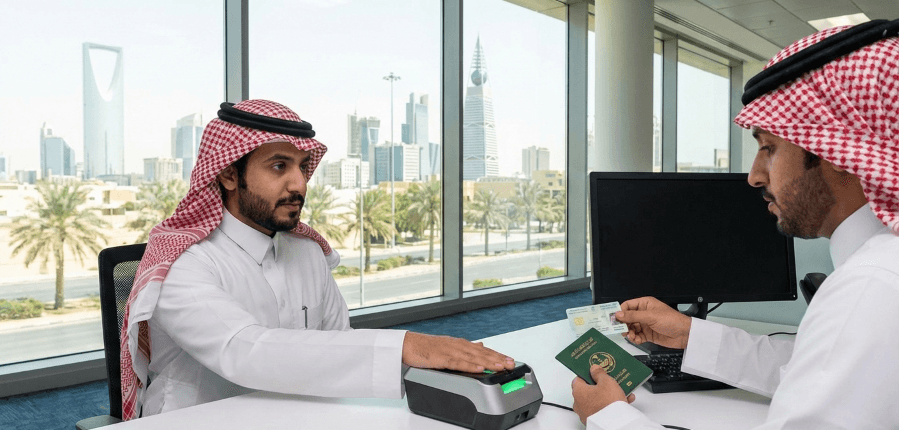

Challenge 3: Remote Onboarding Challenges

Digital channels removed the branch, and along with it the in-person check that used to anchor identity. Now remote onboarding has to prove three things at once: the document is genuine, the person presenting it is its real owner, and neither is a synthetic or stolen identity. All without a human in the room.

This is where video KYC, liveness checks, and phone verification earn their keep. A liveness check confirms a real person is present rather than a photo, video, or deepfake. Document authentication vets the credential itself; matching the selfie to the document binds the person to the identity. Done well, identity verification closes the remote gap fraudsters target most aggressively.

Challenge 4: KYC Screening Challenges

Screening a customer against sanctions lists, politically exposed person (PEP) data, and adverse media sounds straightforward, until you run it at scale. Names transliterate differently across alphabets. Watchlists update constantly. Crude matching logic buries analysts in false positives while risking the one false negative that actually matters.

The fix is matching quality, not raw data volume. Fuzzy matching tuned for transliteration and aliases, deduplicated alerts, and risk-weighted scoring cut the noise so analysts spend their time on real hits. Pair screening at onboarding with ongoing adverse media intelligence and the customer view stays current, not frozen at the moment of signup.

Challenge 5: Sanctions Screening Challenges

Sanctions screening earns its own section because getting it wrong is direct and severe. Regimes change with little warning. Ownership thresholds pull entities into scope through their owners, and a missed match can mean a violation regardless of intent. Over-match instead, and you flood the queue and slow legitimate business.

Good sanctions screening keeps list data fresh, runs at onboarding and continuously after, and applies the relevant ownership and control rules so indirect exposure gets caught. Clear audit trails on every alert decision matter just as much. An examiner will ask not only what you screened but how you resolved each hit.

Challenge 6: UBO and Ownership Challenges

For corporate customers, the hard question is who ultimately owns and controls the entity. Ownership structures span layers of holding companies and jurisdictions. Registry data is inconsistent. And the people who want to hide are precisely the ones building the complexity. Identifying the ultimate beneficial owner ranks among the most labor-intensive parts of KYC, and draws frequent regulatory criticism.

Solving it means unwinding ownership layers to the natural persons behind them, screening each one, then refreshing the picture when structures change. A global KYB solution that maps ownership and applies control thresholds turns a manual investigation into a repeatable, evidenced process.

Regulatory Requirements Behind These Challenges

Most KYC challenges trace back to obligations regulators expect every program to meet:

- Customer identification and verification. Identify and verify customers using reliable, independent sources, typically through a Customer Identification Program and Customer Due Diligence.

- Higher-risk customers get enhanced due diligence: deeper scrutiny of source-of-funds and the purpose of the relationship.

- Ongoing monitoring never stops. Watch transactions and customer activity for unusual or suspicious patterns, and keep watching after onboarding closes.

- Record-keeping. Retain KYC records for at least the FATF-recommended five-year minimum, available to regulators on request.

None of these sits apart from the challenges above. They are the standard the challenges have to be solved against.

Best Practices for Navigating KYC Challenges

A few principles separate programs that scale from programs that stall:

Adopt a risk-based approach so resources concentrate where exposure is highest. Regular customer risk rating lets you reserve enhanced scrutiny for the customers who warrant it and clear the rest efficiently.

Standardize policies and procedures. Identification, verification, and monitoring should run the same way across teams and regions, with clear ownership for each step.

Automate the repetitive work. Document extraction, screening, and risk scoring all suit automation well, which frees analysts for the judgment calls that genuinely require a human.

How KYC Hub Solves KYC Challenges

KYC Hub tackles all six in one platform built for banks and fintechs. The global KYC solution combines video KYC, identity and ID document verification, digital signature, liveness checks, and phone verification so remote onboarding is both fast and defensible. Screening, ongoing monitoring, and UBO discovery run on the same workflow, with full audit trails on every decision.

Since the steps are orchestrated rather than stitched together, low-risk customers clear automatically and analysts spend their time on the real exceptions. The six challenges above stop being recurring fire drills. They become a controlled, evidenced process.